This task can be performed using VolRadar

Daily options analytics for premium sellers

Best product for this task

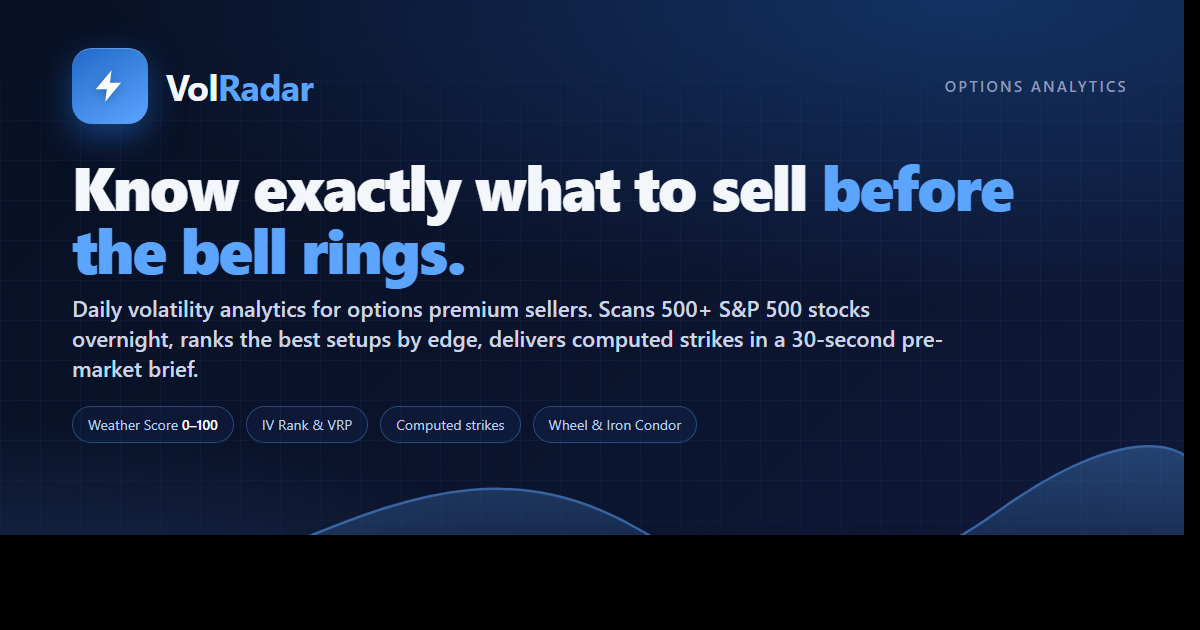

VolRadar

analytics

VolRadar ships a daily pre-market brief for retail options premium sellers — iron condor, credit spread, and wheel traders. Every night after US market close, we pull end-of-day options data from ORATS and compute a Weather Score, IV Rank, VRP, and target-delta strikes across 500+ S&P stocks. By the time you open your broker at 9 AM, you already know which tickers are worth selling. Free forever tier.

options tradingimplied volatilityIV rankVRPpremium sellingthetawheel strategyiron condoroptions analyticsORATS

What to expect from an ideal product

- VolRadar automatically calculates IV Rank for 500+ S&P stocks every night so you don't have to crunch numbers or scan charts manually

- The platform pulls fresh options data from ORATS after market close and delivers a pre-market brief with volatility metrics ready before trading opens

- You get instant access to Volatility Risk Premium (VRP) calculations that would normally take hours to research across multiple tickers

- The Weather Score feature quickly flags which stocks have favorable volatility conditions for selling premium without diving into complex analysis

- Target-delta strikes are pre-calculated and delivered daily, eliminating the guesswork of finding optimal entry points for iron condors and credit spreads